Following on from my last post of “Place your future bets- invest in Innovation Capital” which outlined the significant contribution innovation capital plays in our economic growth and value enhancement, let’s explore some more.

Let me offer some further thoughts on its value to really capture and understand, so we can measure it within our organizations.

We have the three components; of physical capital, knowledge capital and human capital that are the innovation-related assets, these make-up Innovation Capital.

I have been arguing that innovation capital draws from the core of intellectual capital and its suggested (and broadly recognized) components of human, structural and relational capitals or social capital.

I have previously discussed this converging up, as the ‘nesting effect’

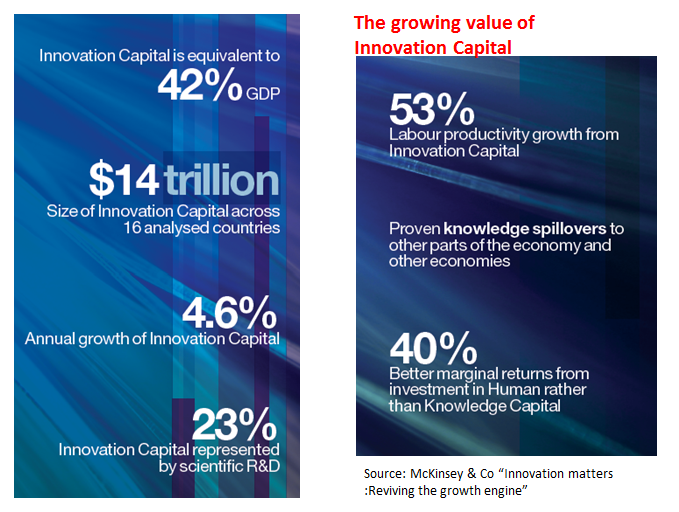

Innovation capital needs assessing and measuring so we can understand the relationship between these innovation capitals (and their present and future potential) and organization performance. We need to know the innovation capital ‘stock’.

Why, well ‘stock’ can be ‘static’ and we need to make this more ‘dynamic’ so innovation can ‘flow’ from this constant renewing of our capitals and be transformed into new value.